Comparison with RadVel#

simppler is very much inspired from the RadVel package.

The goal when writing simppler was actually to test the underlying simpple package on a real use-case, and RadVel seemed like a good comparison (in part because I am familiar with its codebase).

This notebook compares simppler and radvel, on the one hand to make migration between the two easier, and on the other hand to make sure there is no major performance difference between the two.

Data#

We will use the same model and data as in the K2-24 tutorial, as this example was taken from RadVel tutorial.

from pandas import read_csv

import matplotlib.pyplot as plt

url = "https://raw.githubusercontent.com/California-Planet-Search/radvel/refs/heads/master/example_data/epic203771098.csv"

df = read_csv(url, index_col=0)

t = df.t.values

vel = df.vel.values

errvel = df.errvel.values

def plot_data():

plt.figure(figsize=(12, 4))

plt.errorbar(t, vel, yerr=errvel, fmt="k.", capsize=2, mfc="w", label="Data")

plt.xlabel("Time [d]")

plt.ylabel("RV [m/s]")

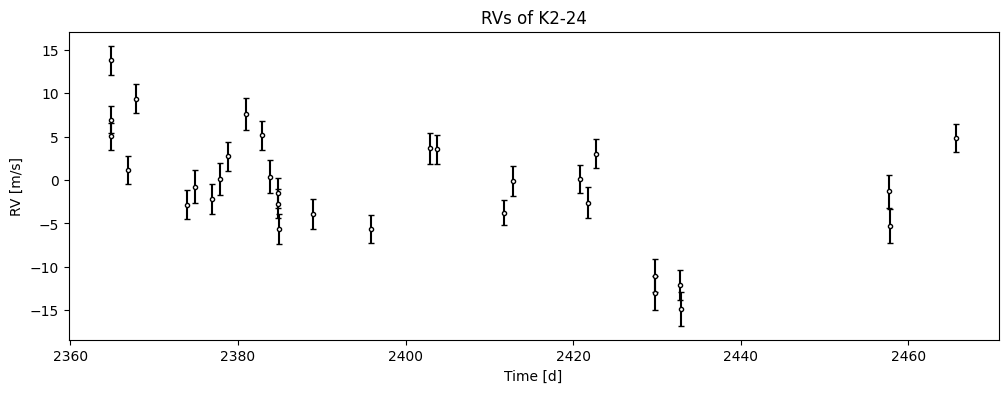

plot_data()

plt.title("RVs of K2-24")

plt.show()

simppler model#

First, we build the simppler, re-using our builder function from the K2-24 tutorial.

import numpy as np

import simppler.model as smod

from simpple import distributions as sdist

periods = [20.8851, 42.3633]

period_errs = [0.0003, 0.0006]

t0s = [2072.7948, 2082.6251]

t0_errs = [0.0007, 0.0004]

def build_model(vary):

if vary == "all":

parameters = {

"per1": sdist.Normal(periods[0], period_errs[0]),

"tc1": sdist.Normal(t0s[0], t0_errs[0]),

"secosw1": sdist.Uniform(-1, 1),

"sesinw1": sdist.Uniform(-1, 1),

"logk1": sdist.Normal(np.log(5), 10),

"per2": sdist.Normal(periods[1], period_errs[1]),

"tc2": sdist.Normal(t0s[1], t0_errs[1]),

"secosw2": sdist.Uniform(-1, 1),

"sesinw2": sdist.Uniform(-1, 1),

"logk2": sdist.Normal(np.log(5), 10),

"dvdt": sdist.Normal(0, 1.0),

"curv": sdist.Normal(0, 1e-1),

"gamma": sdist.Normal(0, 10.0),

"jit": sdist.Normal(np.log(3), 0.5),

}

elif vary == "ecc":

parameters = {

"per1": sdist.Fixed(periods[0]),

"tc1": sdist.Fixed(t0s[0]),

"secosw1": sdist.Uniform(-1, 1),

"sesinw1": sdist.Uniform(-1, 1),

"logk1": sdist.Normal(np.log(5), 10),

"per2": sdist.Fixed(periods[1]),

"tc2": sdist.Fixed(t0s[1]),

"secosw2": sdist.Uniform(-1, 1),

"sesinw2": sdist.Uniform(-1, 1),

"logk2": sdist.Normal(np.log(5), 10),

"dvdt": sdist.Normal(0, 1.0),

"curv": sdist.Normal(0, 1e-1),

"gamma": sdist.Normal(0, 10.0),

"jit": sdist.Normal(np.log(3), 0.5),

}

else:

parameters = {

"per1": sdist.Fixed(periods[0]),

"tc1": sdist.Fixed(t0s[0]),

"secosw1": sdist.Fixed(0.01),

"sesinw1": sdist.Fixed(0.01),

"logk1": sdist.Normal(np.log(5), 10),

"per2": sdist.Fixed(periods[1]),

"tc2": sdist.Fixed(t0s[1]),

"secosw2": sdist.Fixed(0.01),

"sesinw2": sdist.Fixed(0.01),

"logk2": sdist.Normal(np.log(5), 10),

"dvdt": sdist.Normal(0, 1.0),

"curv": sdist.Normal(0, 1e-1),

"gamma": sdist.Normal(0, 10.0),

"jit": sdist.Normal(np.log(3), 0.5),

}

tmod = np.linspace(t.min() - 5, t.max() + 5, num=1000)

time_base = 2420

return smod.RVModel(parameters, 2, t, vel, errvel, basis="per tc secosw sesinw logk", tmod=tmod, time_base=time_base)

simpple_model = build_model("circular")

We will also optimize the model to ensure that we have an easy starting point for the MCMC, as our goal here is not to test sampling efficiency.

test_p = {"per1": periods[0], "tc1": t0s[0], "secosw1": 0.01, "sesinw1": 0.01, "logk1": 1.1}

test_p |= {"per2": periods[1], "tc2": t0s[1], "secosw2": 0.01, "sesinw2": 0.01, "logk2": 1.1}

test_p |= {"gamma": -10, "dvdt": -0.02, "curv": 0.01, "jit": 1.0}

from scipy.optimize import minimize

vary_p = {p: v for p, v in test_p.items() if p in simpple_model.vary_p}

res = minimize(lambda p: - simpple_model.log_prob(p), np.array(list(vary_p.values())), method="Nelder-Mead")

opt_p = dict(zip(simpple_model.keys(), res.x))

Converting from simppler to RadVel#

simppler models have a method allowing us to convert the model directly to a radvel.Posterior object.

radvel_post = simpple_model.to_radvel()

vary_p_arr = [test_p[k] for k in simpple_model.keys()]

radvel_post.set_vary_params(vary_p_arr)

print(radvel_post)

parameter value vary

per1 20.8851 False

tc1 2072.79 False

secosw1 0.01 False

sesinw1 0.01 False

logk1 1.1 True

per2 42.3633 False

tc2 2082.63 False

secosw2 0.01 False

sesinw2 0.01 False

logk2 1.1 True

dvdt -0.02 True

curv 0.01 True

gamma -10 True

jit 1 True

tp1 2070.19

e1 0.0002

w1 0.785398

k1 3.00417

tp2 2077.33

e2 0.0002

w2 0.785398

k2 3.00417

Priors

------

Gaussian prior on logk1, mu=1.6094379124341003, sigma=10

Gaussian prior on logk2, mu=1.6094379124341003, sigma=10

Gaussian prior on dvdt, mu=0, sigma=1.0

Gaussian prior on curv, mu=0, sigma=0.1

Gaussian prior on gamma, mu=0, sigma=10.0

Gaussian prior on jit, mu=1.0986122886681098, sigma=0.5

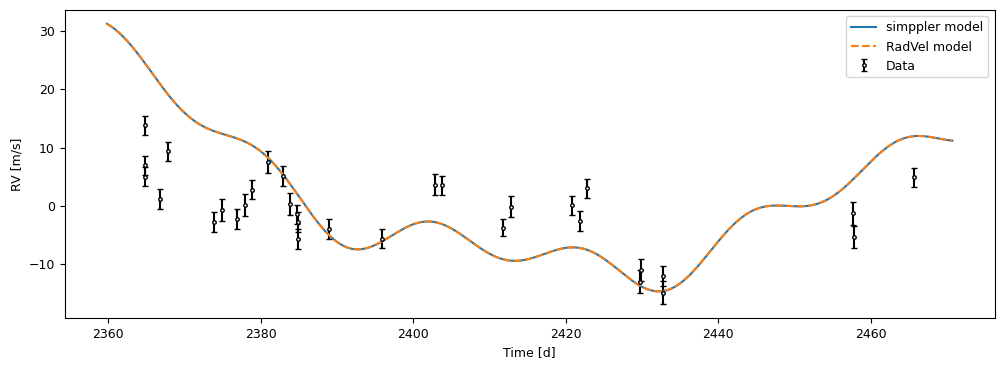

Let us compare the output from the two models

plot_data()

plt.plot(simpple_model.tmod, simpple_model.forward(test_p, simpple_model.tmod), label="simppler model")

plt.plot(

simpple_model.tmod, radvel_post.model(simpple_model.tmod) + radvel_post.params["gamma"].value, "--", label="RadVel model"

)

plt.legend()

plt.show()

That looks good! We can now compare the execution speed of the two models.

Speed comparison#

We do not expect a big performance difference between simppler and radvel: as of writing this, the former uses the keplerian solver from the latter.

However, some performance cost may be associated with the parameter handling or how the distributions are written (this is how I realized that Scipy distributions were quite slow, and switched to custom implementations in simpple).

from timeit import timeit

timeit("radvel_post.logprob_array(vary_p_arr)", globals=globals())

89.83651479500259

For simppler, we will test with dict and array inputs to see if there is a difference.

timeit("simpple_model.log_prob(test_p)", globals=globals())

69.65383110200492

timeit("simpple_model.log_prob(vary_p_arr)", globals=globals())

75.79917559599562

As expected, everything here is fairly similar.

Sampling comparison#

We can also compare the sampling results from the two packages to ensure that they are consistent.

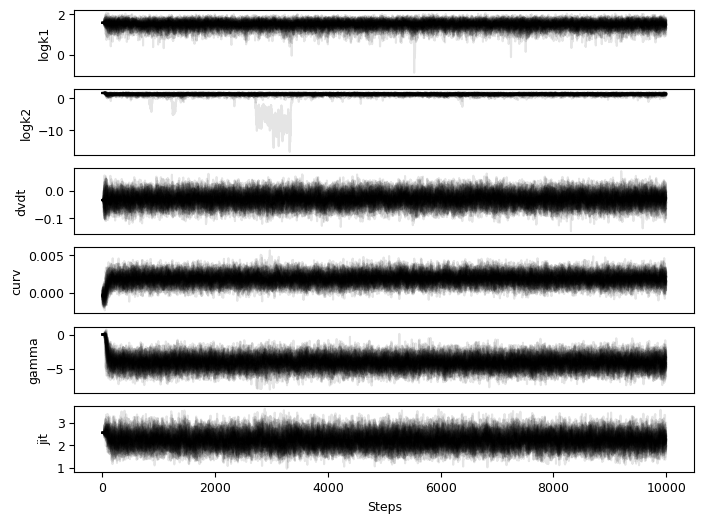

simppler sampling#

import emcee

nwalkers = 50

nsteps = 10_000

ndim = simpple_model.ndim

sampler = emcee.EnsembleSampler(nwalkers, ndim, simpple_model.log_prob)

rng = np.random.default_rng()

p0 = res.x + 1e-4 * rng.normal(size=(nwalkers, ndim))

_ = sampler.run_mcmc(p0, nsteps, progress=True)

from simpple.plot import chainplot

chainplot(sampler.get_chain(), labels=simpple_model.keys())

plt.show()

import corner

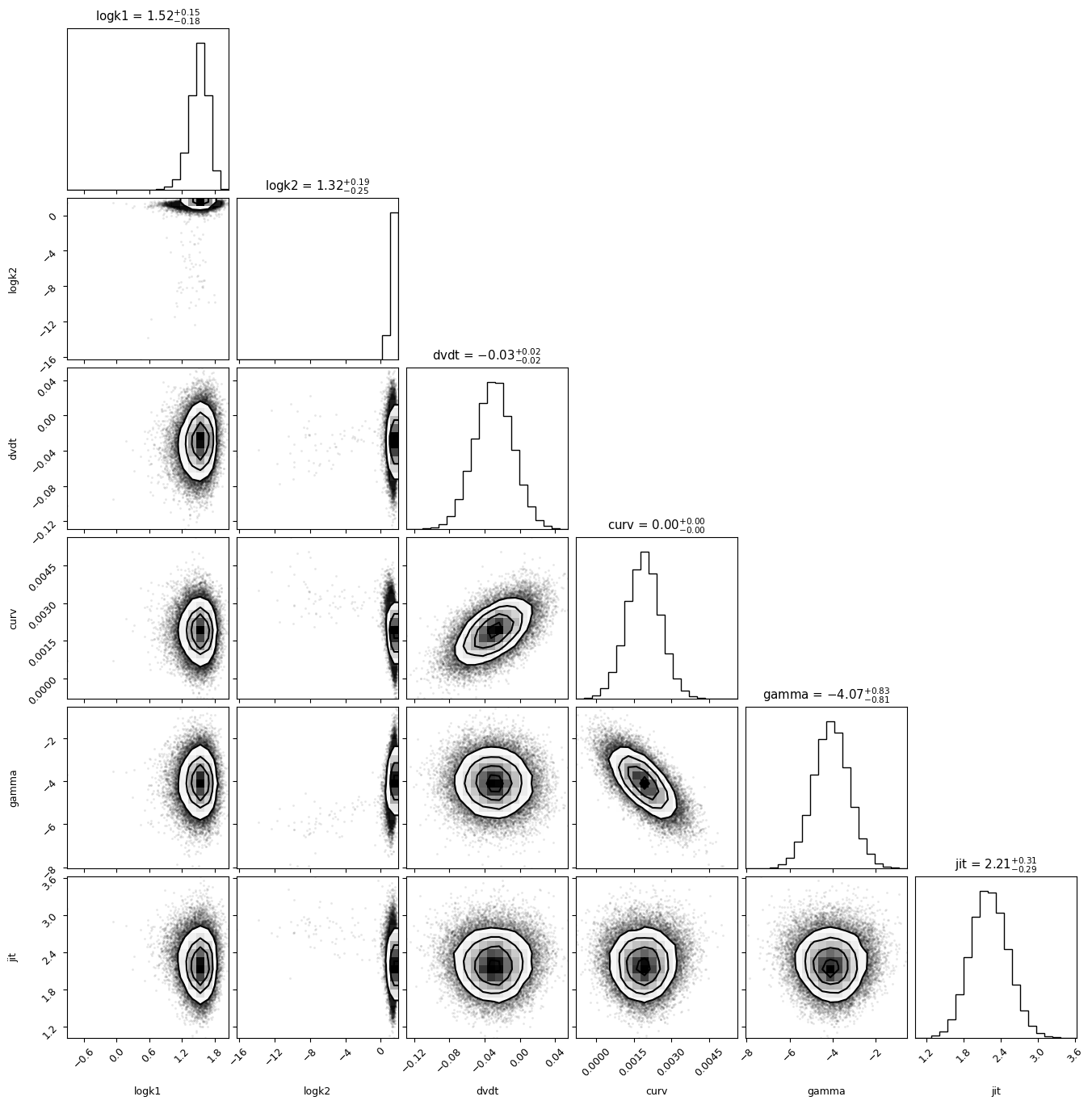

simppler_chains = sampler.get_chain(discard=2000, flat=True, thin=10)

corner.corner(simppler_chains, labels=simpple_model.keys(), show_titles=True)

plt.show()

WARNING:root:Too few points to create valid contours

radvel sampling#

import emcee

sampler = emcee.EnsembleSampler(nwalkers, ndim, radvel_post.logprob_array)

_ = sampler.run_mcmc(p0, nsteps, progress=True)

from simpple.plot import chainplot

chainplot(sampler.get_chain(), labels=radvel_post.name_vary_params())

plt.show()

import corner

radvel_chains = sampler.get_chain(discard=2000, flat=True, thin=10)

corner.corner(radvel_chains, labels=radvel_post.name_vary_params(), show_titles=True)

plt.show()

WARNING:root:Too few points to create valid contours

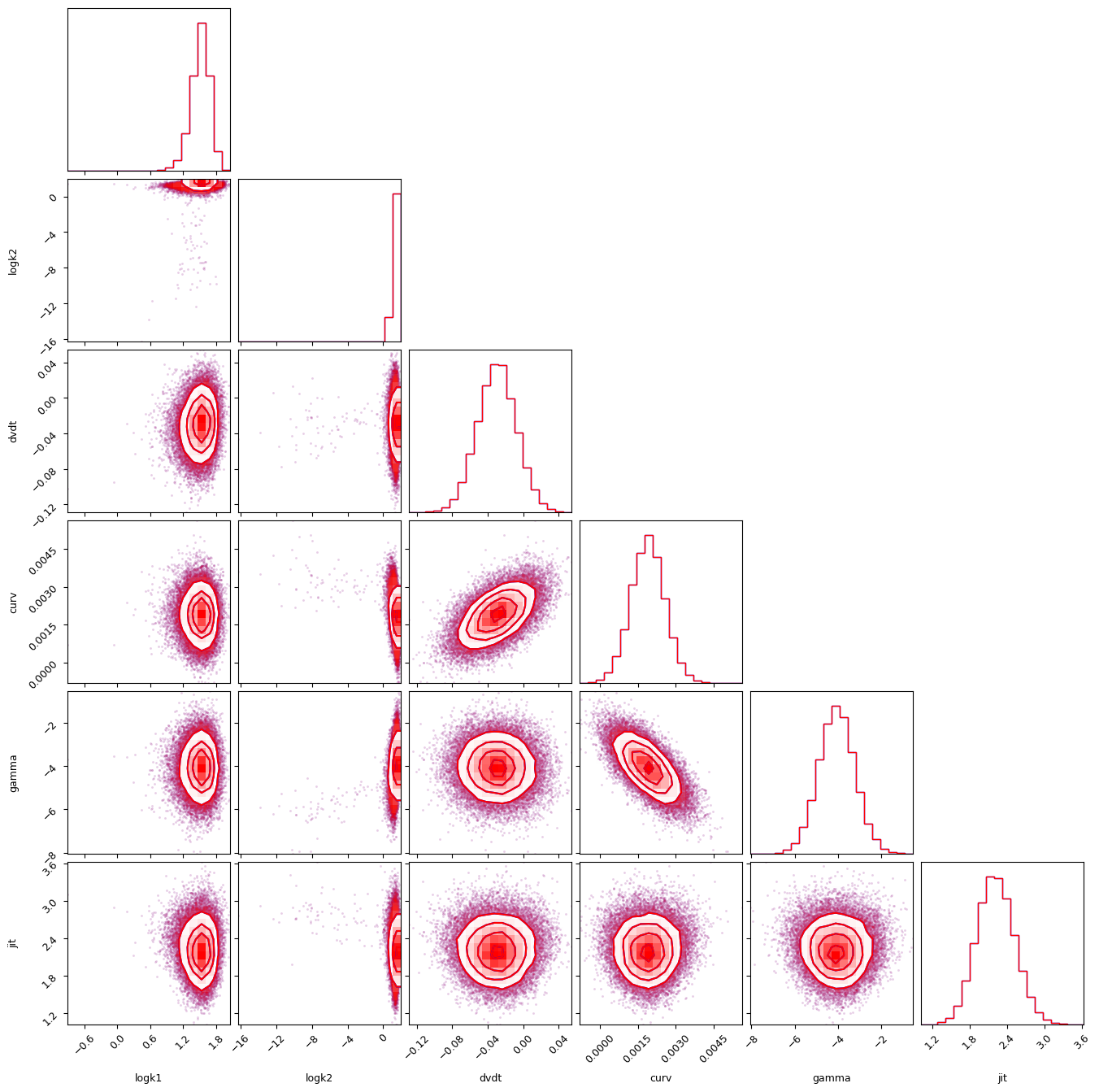

Combined corner plot#

import corner

fig = corner.corner(radvel_chains, labels=radvel_post.name_vary_params(), color="b")

corner.corner(simppler_chains, color="r", fig=fig)

plt.show()

WARNING:root:Too few points to create valid contours

WARNING:root:Too few points to create valid contours